Page 2 of 2

Re: Structure Break in Variance Equation of MGARCH

Posted: Sun Dec 13, 2020 11:28 am

by TomDoan

You have *really* serious issues. The t parameter can't be below 2 (actually can't even be 2), so that is right at the edge of the defined parameter range. It seems like your data are dominated by massive outliers that a GARCH model can't even come close to explaining.

Re: Structure Break in Variance Equation of MGARCH

Posted: Sun Dec 13, 2020 11:37 am

by prashantj

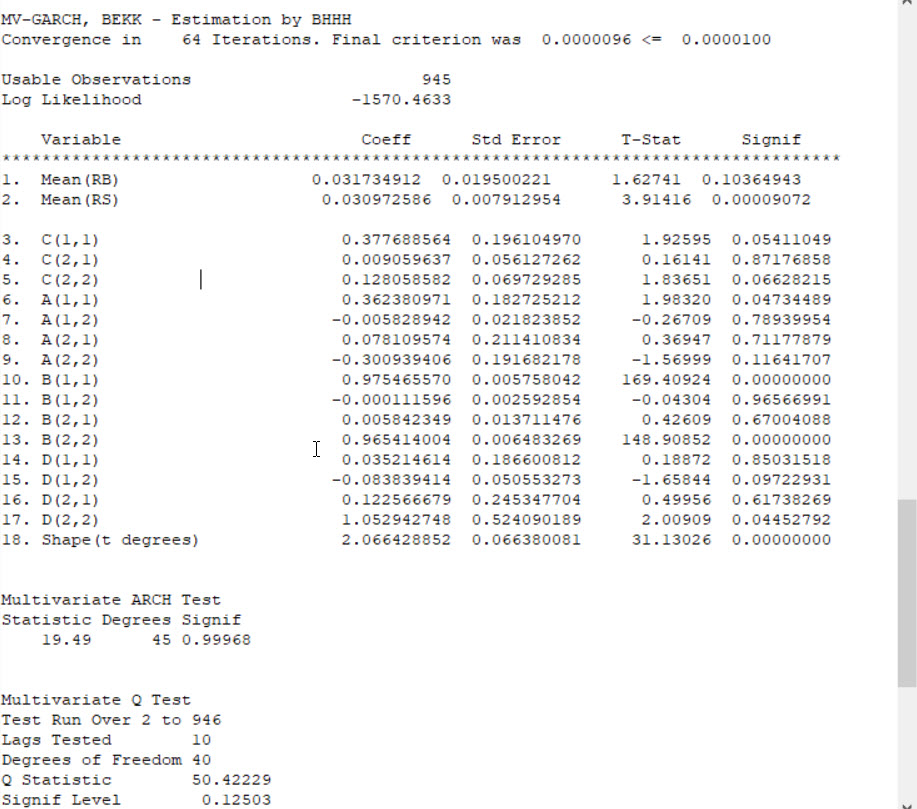

thanks. When I change the method=BHHH, I have got the estimate. Here is the output. But as you said GARCH model can't explain the massive outlier, which tool should I use to analyze such dataset if GARCH can't handle it? I am sorry to ask but this always is a big challenge when I every tried to estimate MGARCH volatility. It takes so much of efforts.

- output1.jpg (232.39 KiB) Viewed 18351 times

Re: Structure Break in Variance Equation of MGARCH

Posted: Mon Dec 14, 2020 6:15 am

by TomDoan

The first is to make sure that the outliers are actually "outliers" and not some form of typo or non-trading "price".

The jump-GARCH model is an alternative which allows for discrete jumps which don't really interact with an underlying GARCH process.

Re: Structure Break in Variance Equation of MGARCH

Posted: Mon Dec 14, 2020 11:06 am

by prashantj

Amazing! Thanks. I really appreciate your insight always. It really helpful and useful.

I have another question if we have a command to sort rows such as to find days with similar prices or no prices or something like that to know non-trading days, that might not be perfect way to identify but helps a lot in saving time and efforts, with massive dataset

Re: Structure Break in Variance Equation of MGARCH

Posted: Mon Dec 14, 2020 2:07 pm

by TomDoan

Wouldn't that just be zero returns? That doesn't necessarily mean that there are no trades, but it isn't uncommon for price series to be patched with the previous day's price if there is no activity.

Re: Structure Break in Variance Equation of MGARCH

Posted: Tue Dec 15, 2020 11:10 am

by prashantj

Hi Tom,

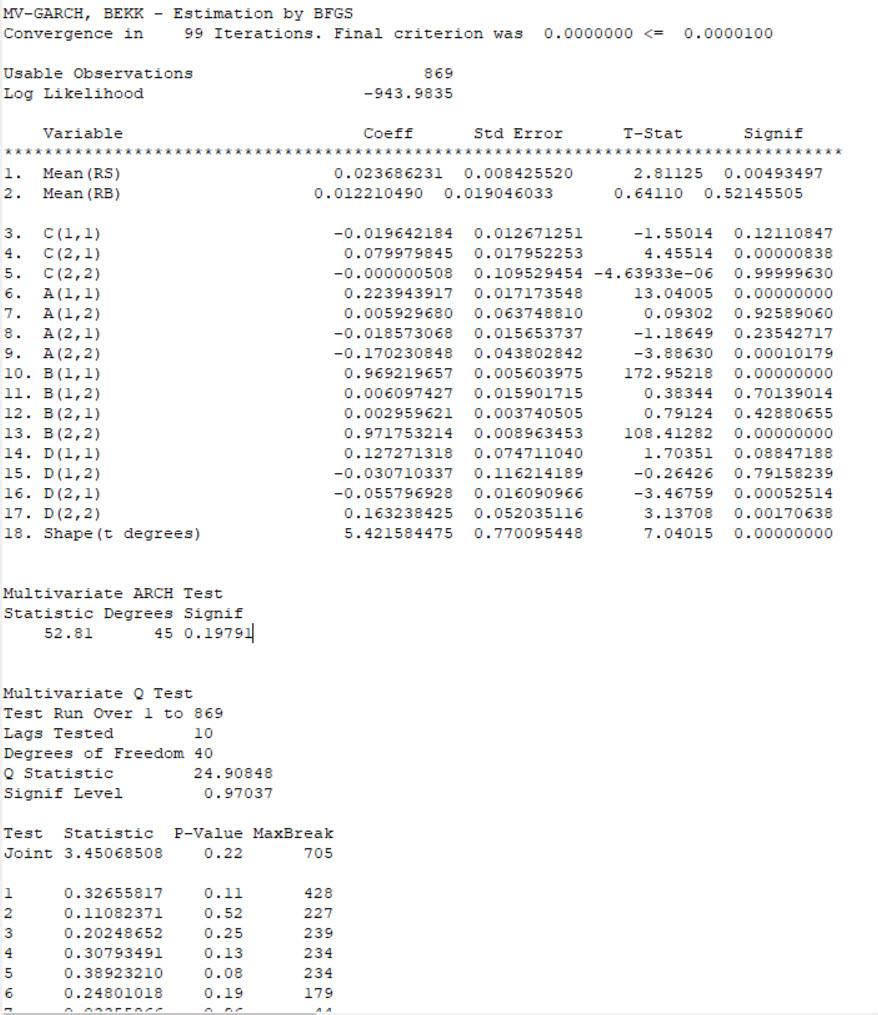

Thanks for your suggestion. I detected and adjusted for zero return and this is the output I got. It looks reasonable? please

- output1.jpg (263.87 KiB) Viewed 18333 times

Re: Structure Break in Variance Equation of MGARCH

Posted: Tue Dec 15, 2020 11:57 am

by TomDoan

That looks like a well-behaved GARCH model.

Re: Structure Break in Variance Equation of MGARCH

Posted: Thu Dec 17, 2020 6:45 pm

by prashantj

TomDoan wrote:That looks like a well-behaved GARCH model.

So, I attempted the forecasting of it and the graph looks like this. Does it mean the forecasting appear to be reasonable and converging to low volatility towards the average?

Re: Structure Break in Variance Equation of MGARCH

Posted: Thu Dec 17, 2020 8:56 pm

by TomDoan

Whether it's a well-fitting GARCH model or not, that's the behavior of the out-of-sample variance forecasts of a GARCH process.

Re: Structure Break in Variance Equation of MGARCH

Posted: Thu Dec 17, 2020 9:03 pm

by prashantj

Thanks. Is it possible in MGARCH to estimate and compare in-sample and out of sample forecast? How do we compare it to see that the fitted model is a better model?

Re: Structure Break in Variance Equation of MGARCH

Posted: Thu Dec 17, 2020 9:19 pm

by TomDoan

Not really. Volatility isn't observable so you don't really have a standard for comparison.

Re: Structure Break in Variance Equation of MGARCH

Posted: Thu Dec 17, 2020 9:23 pm

by prashantj

Okay. So I just report what I have in out of sample volatility forecasting? and it is not possible to know how good that forecasting is despite the good model as suggested by MARCH and Q, fluctuations tests ?

Re: Structure Break in Variance Equation of MGARCH

Posted: Fri Dec 18, 2020 11:50 am

by TomDoan

You can read about the problems with evaluating GARCH forecasts in the

Jan 2018 newsletter.

Re: Structure Break in Variance Equation of MGARCH

Posted: Fri Dec 18, 2020 12:15 pm

by prashantj

Wonderful! Thanks.