Page 3 of 3

Re: negative coefficients of ARCH terms in MGARCH-BEKK

Posted: Wed Nov 25, 2020 12:08 pm

by TomDoan

There's no way I could tell from that. Have you even graphed your data? You should know whether there are issues even before you fit a model.

Re: negative coefficients of ARCH terms in MGARCH-BEKK

Posted: Wed Nov 25, 2020 2:21 pm

by prashantj

This is what I got there are some outliers, but these are what I think we find with GARCH series?

Re: negative coefficients of ARCH terms in MGARCH-BEKK

Posted: Thu Nov 26, 2020 1:51 am

by prashantj

Finally, I think I have got the following model with my intraday data after adjusting for outliers, took a long! . I hope that is a good model, Tom?

- SPill.jpg (235.52 KiB) Viewed 13948 times

Re: negative coefficients of ARCH terms in MGARCH-BEKK

Posted: Sat Nov 28, 2020 10:48 am

by TomDoan

That looks more reasonable.

Re: negative coefficients of ARCH terms in MGARCH-BEKK

Posted: Sat Nov 28, 2020 11:41 am

by TomDoan

prashantj wrote:This is what I got there are some outliers, but these are what I think we find with GARCH series?

Graph.RGF

The series is black seems to have a quite a few big outliers of opposite signs in close proximity (possibly adjacent entries) with no apparent effect on volatility subsequent to that. That tends to be a sign of either a one data point typo in the price series or some other move and immediate correction that is seen in the market as an obvious fix.

Re: negative coefficients of ARCH terms in MGARCH-BEKK

Posted: Sat Nov 28, 2020 2:35 pm

by prashantj

Thanks , Tom. I appreciate it. I seen quite great features in RATS10. The computational power has improved significantly much faster than older version 8.2 I had. RATS saves a significance time in learning and looking for program like using open source softwares. And your help makes RATS unique. When the RATS11 you plan to release? I will be the first to get it.

Thanks!

Prashant

Re: negative coefficients of ARCH terms in MGARCH-BEKK

Posted: Tue Dec 01, 2020 10:28 am

by prashantj

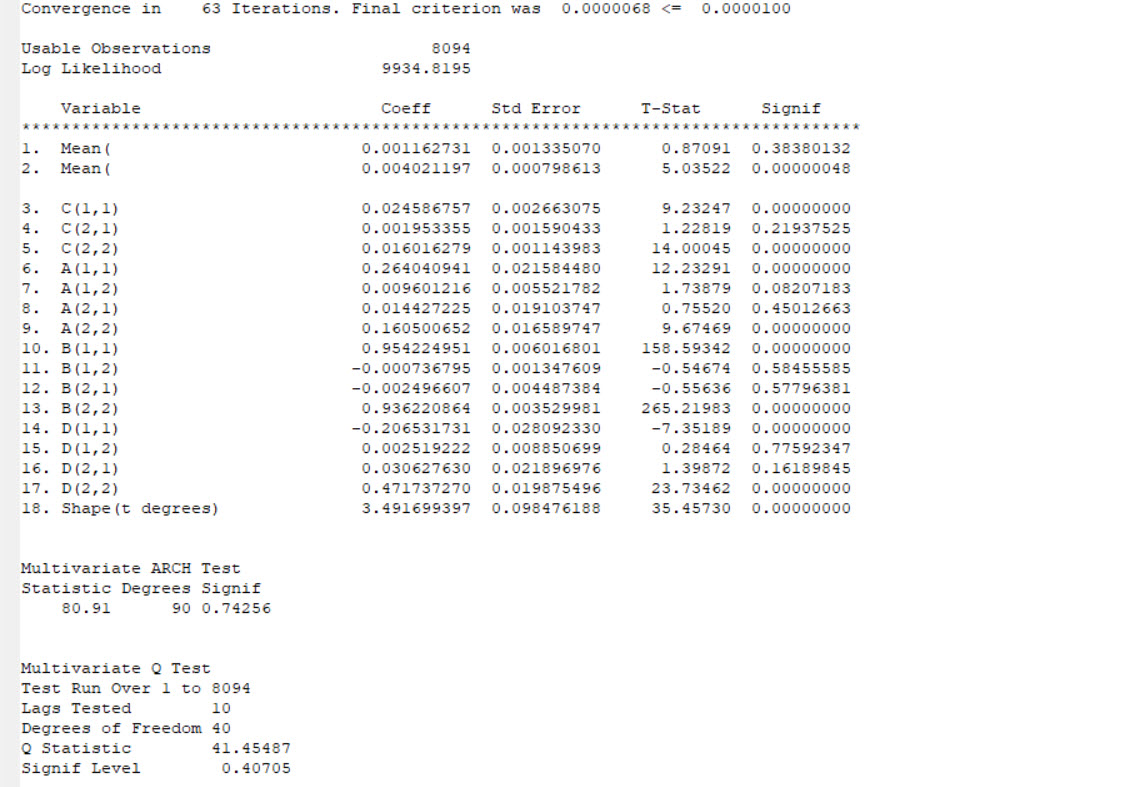

I was estimating BEKK MGARCH model by creating variance dummy using the procedure discussed in GARCH course workbook in Section 6.3 and I got the following output (am attaching truncated). I would like to get value for march(1,2). Is it possible to generate?

garch(mv=BEKK,rvectors=rd,hmatrices=hh,pmethod=simplex,asymmetric,xreg,stdresids=rstd,piters=20,iters=500,dist=T) / rsp rbg

# march19

- dummy.jpg (41.9 KiB) Viewed 13934 times

Re: negative coefficients of ARCH terms in MGARCH-BEKK

Posted: Tue Dec 01, 2020 10:41 am

by TomDoan

It's a lower triangular matrix (has to be---a full 2x2 matrix wouldn't be identified) so the 1,2 element is zero.

Re: negative coefficients of ARCH terms in MGARCH-BEKK

Posted: Tue Dec 01, 2020 12:01 pm

by prashantj

got it. Thanks.

Prashant

Re: negative coefficients of ARCH terms in MGARCH-BEKK

Posted: Wed Dec 02, 2020 7:26 pm

by prashantj

Is till could not import intraday data with the time stamps. I tried all possibilies I can but of no avail. can you please help me with it to read the data in RATS10? I will send you the file.

Looking forward for your reply,

Prashant