Page 1 of 1

RE:Cross volatility

Posted: Wed Jun 21, 2017 12:01 pm

by veryconfusedmgarch

Hi,

I am new to RATS and I have a question on how to estimate the following specification within RATS.

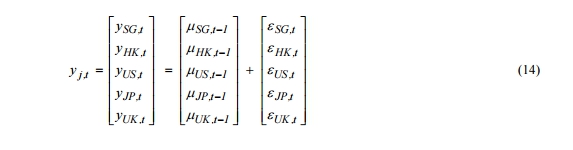

The conditional mean equation is,

- Mean equation

- screenshot.543.jpg (27.15 KiB) Viewed 14336 times

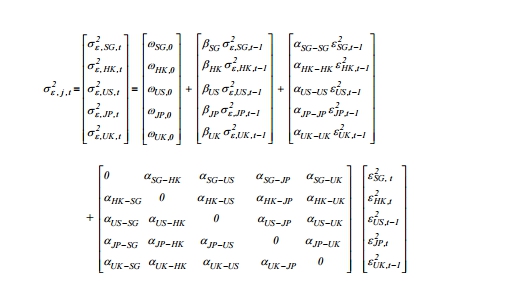

And the conditional variance is

- Conditional Variance

- screenshot.542.jpg (75.42 KiB) Viewed 14336 times

Note that some errors are comtemperneous i.e. SG, HK and JP and errors of UK and US are lagged one period.

I understand how to estimate a VAR-BEKK-MGARCH model with RATS, but I am not so sure how to recover the alphas in the 5x5 matrix of the conditional variance equations, as well as how to adjust for the lagged and comtemperneous errors (i.e. the last term in the variance equation)

I appreciate your help in advance!

Re: RE:Cross volatility

Posted: Wed Jun 21, 2017 12:39 pm

by TomDoan

I assume that's a timing issue? That's definitely not BEKK---if it weren't for the t vs t-1's in the last matrix, this would be the VARIANCES=SPILLOVER model. You have a model for the variances, but what about the covariances? CC or DCC?

Re: RE:Cross volatility

Posted: Wed Jun 21, 2017 2:36 pm

by veryconfusedmgarch

TomDoan wrote:I assume that's a timing issue? That's definitely not BEKK---if it weren't for the t vs t-1's in the last matrix, this would be the VARIANCES=SPILLOVER model. You have a model for the variances, but what about the covariances? CC or DCC?

Yes, it's definitely not BEKK - I just meant that I know the basis for estimating BEKK under RATS package. Sorry for the missing information, the covariance is CC.

Thanks Tom!

Re: RE:Cross volatility

Posted: Wed Jun 21, 2017 3:28 pm

by TomDoan

That's sufficiently non-standard that it would have to be done using MAXIMIZE. I'm a bit unsure about how that works though. Why wouldn't the squared terms for Asian markets on each other be lagged? I understand US and UK on current Asian markets, but not using current Asian markets throughout. (Formula isn't as pretty, but that seems more realistic).

Re: RE:Cross volatility

Posted: Wed Jun 21, 2017 5:19 pm

by veryconfusedmgarch

TomDoan wrote:That's sufficiently non-standard that it would have to be done using MAXIMIZE. I'm a bit unsure about how that works though. Why wouldn't the squared terms for Asian markets on each other be lagged? I understand US and UK on current Asian markets, but not using current Asian markets throughout. (Formula isn't as pretty, but that seems more realistic).

Hi Tom,

Thanks for your reply. It is because of the time zone differences between US/UK and JP/HK/SG and hence more realistic, but also makes the formula messier. Could you please let me know maybe a similar example using maximize so that I can try and make the relevant changes to estimate the model?

I appreciate your help and patient!

Thank you.

Re: RE:Cross volatility

Posted: Thu Jun 22, 2017 2:28 pm

by TomDoan

This will estimate the model of interest. I changed the data file name and guessed at which indices were which, so you want to double check that---I would suggest that you either put some more descriptive names than S1, S2, ... on the data, or put in a separate sheet with descriptions.

The non-standard timing of the spillovers is covered by:

input uutiming

1 0 1 0 1

0 1 1 0 1

0 0 1 0 1

0 0 1 1 1

0 0 1 0 1

This combines both the own and cross effects into a single matrix. A row corresponds to the variance being computed (in the same order as you give) and the columns correspond to the squared eps's. A 1 means to use t-1 and a 0 means to use t.