|

Examples / DSGEKPR.RPF |

DSGEKPR.RPF is an example of the solution of a non-linear DSGE model. This demonstrates the DSGE instruction and the @DLMIRF procedure.

Watson (1993) analyzes a special case of the model below (with some minor renaming of variables) whose equilibrium is described by the following equations:

\begin{equation} \frac{\theta }{{1 - N_t }} = C_t^{ - \eta } \alpha \frac{{Y_t }}{{N_t }} \end{equation}

\begin{equation} 1 = \beta \gamma ^{1 - \eta } E_t R_{t + 1} \left( {{{C_t } \mathord{\left/ {\vphantom {{C_t } {C_{t + 1} }}} \right. } {C_{t + 1} }}} \right)^\eta \end{equation}

\begin{equation} \gamma R_t = \left( {1 - \alpha } \right)\frac{{Y_t }}{{K_{t - 1} }} + 1 - \delta \end{equation}

\begin{equation} C_t + I_t = Y_t \end{equation}

\begin{equation} \gamma K_t = I_t + \left( {1 - \delta } \right)K_{t - 1} \end{equation}

\begin{equation} Y_t = Z_t K_{t - 1}^{1 - \alpha } N_t^\alpha \end{equation}

\begin{equation} \log Z_t = \left( {1 - \rho } \right)\log \left( {\bar Z} \right) + \rho \log \left( {Z_{t - 1} } \right) + \varepsilon _t \label{eq:dsgekpr_eq7} \end{equation}

There is only one exogenous shock in this model (equation \eqref{eq:dsgekpr_eq7}—the technology shock). This is a non-linear model, which will be analyzed using a log-linearization. Because \(N\) (labor force participation rate) can’t take the value 1, we can’t use the default initial guess values for all variables, so the initial values parameters are used for some. SOLVEBY=SVD is included to deal with the unit root in the technology shock.

This is the King-Plosser-Rebelo(1988) model, hence the name of the program. However, the date conventions for capital are those recommended by Uhlig and Sims, rather than KPR's.

open data watson_jpe.rat

calendar(q) 1948:1

data(format=rats) 1948:1 1988:4 y c invst h

Several of the series used in the model are unobservable and so aren’t in the data set (which is never actually used in this example). They’re included in a DECLARE SERIES instruction so they can be used in defining the equations.

declare series n r z k

declare real theta eta alpha beta gamma delta psi

These are the calibration values used by Watson.

compute eta=1.0 Log utility

compute alpha=.58 Labor’s share

compute nbar=.2 Steady state level of hours

compute gamma=1.004 Rate of technological progress

compute delta=.025 Depreciation rate for capital (quarterly)

compute rq=.065/4 Quarterly steady state interest rate

compute rho=1.00 AR coefficient in technical change

compute lrstd=.01 Long-run standard deviation of output

compute zbar=1.0 Mean of technology process

compute theta=3.29 Preference parameter for leisure

compute beta=gamma/(1+rq)

Define the equations. F7 is the only one with a shock attached. F2 is the only one with an expectational term (for future \(C\) and future \(R\)).

frml(identity) f1 = theta/(1-n)-c^(-eta)*alpha*y/n

frml(identity) f2 = 1-beta*gamma^(1-eta)*c/c{-1}*r{-1}

frml(identity) f3 = gamma*r-(1-alpha)*y/k{1}-1+delta

frml(identity) f4 = c+invst-y

frml(identity) f5 = gamma*k-invst-(1-delta)*k{1}

frml(identity) f6 = y-z*k{1}^(1-alpha)*n^alpha

frml f7 = log(z)-(1-rho)*log(zbar)-rho*log(z{1})

group swmodel f1 f2 f3 f4 f5 f6 f7

Solve the model to state-space form, overriding several settings for the guess values.

dsge(model=swmodel,expand=loglinear,a=a,f=f,solveby=svd) $

y c<<0.5 invst<<0.5 n<<nbar r<<1+rq k z

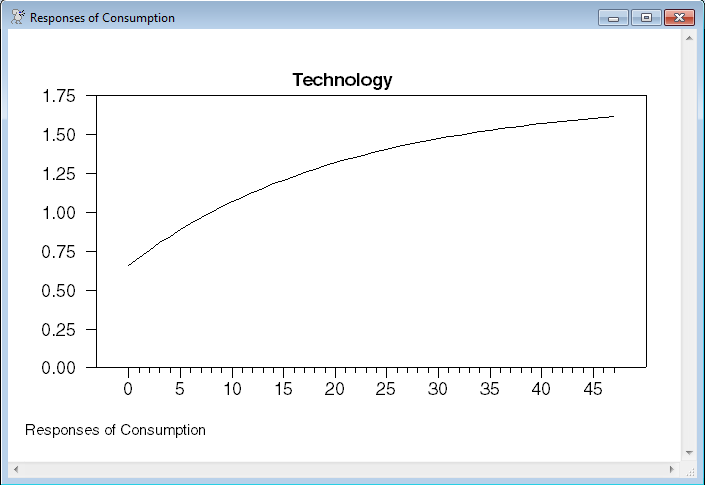

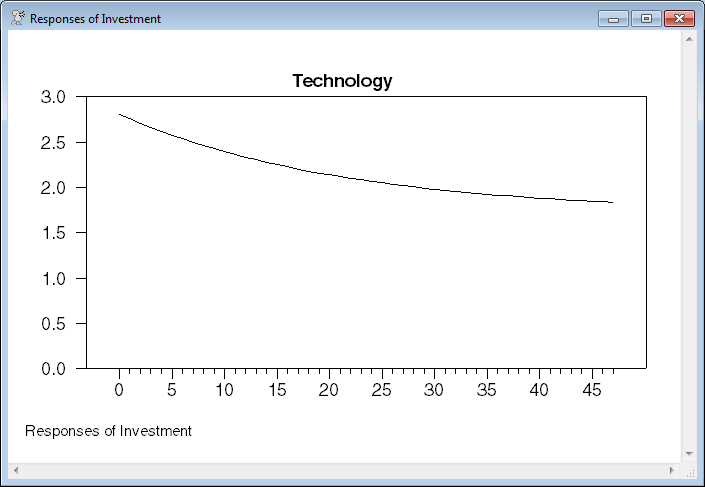

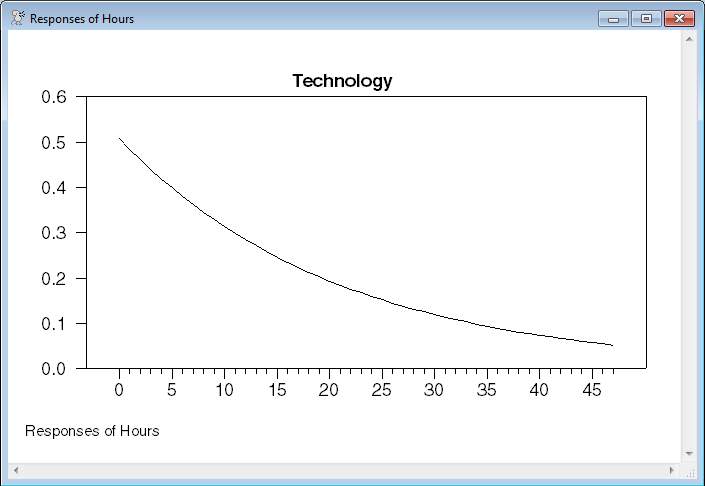

Graph the impulse responses using the state-space matrices. The state-space model will have more than four states, but by limiting the VARIABLES option, you only see the four main ones, and not R, K, Z and any augmenting states.

@dlmirf(a=a,f=f,graph=byvar,shocks=||"Technology"||,$

variables=||"Output","Consumption","Investment","Hours"||)

Full Program

*

* Replication program for Watson (1993), "Measures of Fit for Calibrated

* Models", J. of Political Economy, vol 101, pp 1011-1041. This uses the

* model from King, Plosser and Rebelo, but with the date conventions

* used by Uhlig and Sims, rather than KPR's.

*

* Get data. Income, consumption and investment are log real per capita

* values.

*

open data watson_jpe.rat

cal(q) 1948

data(format=rats) 1948:1 1988:4 y c invst h

*

* theta/(1-N(t))=C(t)^(-eta)alpha*Y(t)/N(t)

* 1=(beta-star)*Et[(C(t)/C(t+1))^eta R(t+1)], where beta-star=beta*gamma^(1-eta)

* gamma R(t)=(1-alpha)*Y(t)/K(t-1)+1-delta

*

* with

*

* C(t)+I(t)=Y(t)

* gamma K(t)=I(t)+(1-delta)*K(t-1)

* Y(t)=Z(t)*K(t-1)^(1-alpha)*N(t)^alpha

* log Z(t)=(1-psi)*log(Z-bar)+psi*log(Z(t-1))+eps(t)

*

* Several of the series used in the model are unobservable and so aren’t

* in the data set. (The data aren't used in this short example). They’re

* included in a DECLARE SERIES instruction so they can be used in

* defining the equations.

*

declare series n r z k

*

declare real theta eta alpha beta gamma delta psi

*

* Calibration values used by Watson

*

compute eta=1.0 ;* Log utility

compute alpha=.58 ;* Labor's share

compute nbar=.2 ;* Steady state level of hours (used in place of "A" in utility function)

compute gamma=1.004 ;* Rate of technological progress

compute delta=.025 ;* Depreciation rate for capital (quarterly)

compute rq=.065/4 ;* Quarterly steady state interest rate

compute rho=1.00 ;* AR coefficient in technical change

compute lrstd=.01 ;* Long-run standard deviation of output

compute zbar=1.0 ;* Mean of technology process

compute theta=3.29 ;* Preference parameter for leisure

compute beta=gamma/(1+rq)

compute sigma=lrstd*alpha

*

* Define the equations. F7 is the only one with a shock attached. F2 is

* the only one with an expectational term (for future C).

*

frml(identity) f1 = theta/(1-n)-c^(-eta)*alpha*y/n

frml(identity) f2 = 1-beta*gamma^(1-eta)*c/c{-1}*r{-1}

frml(identity) f3 = gamma*r-(1-alpha)*y/k{1}-1+delta

frml(identity) f4 = c+invst-y

frml(identity) f5 = gamma*k-invst-(1-delta)*k{1}

frml(identity) f6 = y-z*k{1}^(1-alpha)*n^alpha

frml f7 = log(z)-(1-rho)*log(zbar)-rho*log(z{1})

*

group swmodel f1 f2 f3 f4 f5 f6 f7

*

* Solve the model to state-space form, overriding several settings for

* the guess values.

*

dsge(model=swmodel,expand=loglinear,a=a,f=f,solveby=svd) $

y c<<0.5 invst<<0.5 n<<nbar r<<1+rq k z

*

* Graph the impulse responses using the state-space matrices. The

* state-space model will have more than four states, but by limiting the

* VARIABLES option, you only see the four main ones, and not R, K, Z and

* any augmenting states.

*

@dlmirf(a=a,f=f,page=byvar,shocks=||"Technology"||,$

variables=||"Output","Consumption","Investment","Hours"||)

Graphs

Copyright © 2026 Thomas A. Doan