|

Examples / EXPSMOOTH1.RPF |

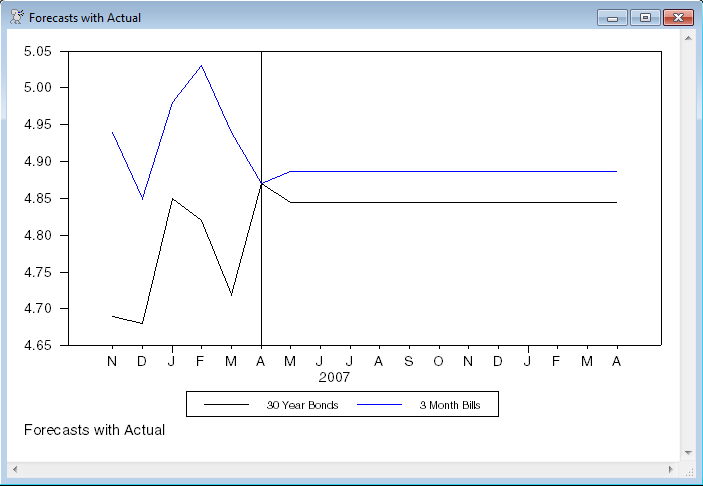

EXPSMOOTH1.RPF demonstrates the use of the ESMOOTH instruction for exponential smoothing. It does out-of-sample forecasts for monthly data on US 30 year Treasury Bonds (FCM30) and 3-month Treasury Bills (FTBS3).

These forecast 12 steps out, using a simple smoothing model with a fixed parameter of .8. It appends the forecasts to the series for ease in graphing:

esmooth(alpha=.8,forecast=ftbs3,steps=12) ftbs3

esmooth(alpha=.8,forecast=fcm30,steps=12) fcm30

This does a graph with more informative key labels, showing the last six months of actual data, followed by the forecasts. It includes a vertical line at 2007:4 (the end of actual data).

graph(grid=(t==2007:4),key=below, $

klabels=||"30 Year Bonds","3 Month Bills"||) 2

# fcm30 2006:11 2008:4

# ftbs3 2006:11 2008:4

Full Program

open data haversample.rat

calendar(m) 1978

data(format=rats) 1978:1 2007:4 fcm30 ftbs3

*

* FCM30 = Yield on 30 Year Treasury Bonds

* FTBS3 = Yield on 3 Month Treasury Bills

*

* Forecast twelve periods out-of-sample using simple smoothing model

* with fixed parameter of .8. Append the forecasts to the series for

* ease in graphing.

*

esmooth(alpha=.8,forecast=ftbs3,steps=12) ftbs3

esmooth(alpha=.8,forecast=fcm30,steps=12) fcm30

*

* Graph with more informative key labels, showing the last six months of

* actual data, followed by the forecasts. Include a vertical line at

* 2007:4.

*

graph(grid=(t==2007:4),key=below,footer="Forecasts with Actual", $

klabels=||"30 Year Bonds","3 Month Bills"||) 2

# fcm30 2006:11 2008:4

# ftbs3 2006:11 2008:4

Graph

Copyright © 2026 Thomas A. Doan