|

Examples / GIBBSPROBITDYNAMIC.RPF |

GIBBSPROBITDYNAMIC.RPF shows how to get a Gibbs sampling estimate of a dynamic "probit" model, where the latent index follows an AR(1) equation:

\(y_t^* = \alpha + \rho y_{t - 1}^* + {\varepsilon _t},{\text{ with }}{\varepsilon _t}\sim N\left( {0,1} \right){\rm{ }}i.i.d.\)

This uses the typical Gibbs sampling technique of drawing the continuous latent variable given the observable 0-1's, but, because of the dynamic process for the latent variable, you can't just draw those independently. Instead, the YSTAR are done one-at-a-time given the values of the YSTAR at all other data points.

Full Program

cal(q) 1960

@nbercycles(up=expansion) 1960:1 2009:4

*

* Start with ystar of +/-1

*

set ystar = %if(expansion,1.0,-1.0)

*

* Start the sampler at the OLS estimates, given the starting ystars

*

linreg ystar

# constant ystar{1}

compute rho=%beta(2),alpha=%beta(1)

*

* Set up state space model for ystar

*

frml af = rho

frml zf = alpha

*

* (diffuse) prior for coefficients

*

compute bprior=%zeros(2,1)

compute hprior=%zeros(2,2)

*

compute nburn=1000

compute ndraws=1000

*

dec series[vect] bgibbs

gset bgibbs 1 ndraws = %zeros(2,1)

set ystarhat = 0.0

*

infobox(action=define,progress,lower=-nburn,upper=ndraws) "Gibbs Sampler: Dynamic Probit"

do draw=-nburn,ndraws

infobox(current=draw)

*

* Draw ystar(time) given all other ystar's. This is done by Gibbs

* sampling on

*

* ystar(t)=alpha+rho*ystar(t-1)+eps(t) (state equation)

* ystar(t)=ystar(t)+0 if t<>time (measurement equation)

*

* Kalman smoothing gives the conditional mean and variance for

* ystar(time).

*

do time=1960:1,2009:4

dlm(y=%if(t==time,%na,ystar),a=af,z=zf,c=1.0,$

sw=1.0,presample=ergodic,type=smooth) 1960:1 2009:4 xstates vstates

compute cmean=%scalar(xstates(time)),cstddev=sqrt(%scalar(vstates(time)))

*

* Given the conditional mean and the observed value for the 0-1

* variable, draw a truncated Normal for ystar.

*

compute ystar(time)=%if(expansion(time),%rantruncate(cmean,cstddev,0.0,%na),$

%rantruncate(cmean,cstddev,%na,0.0))

end do time

*

* Draw coefficients from the index equation given ystars

*

cmom

# constant ystar{1} ystar

compute bdraw=%ranmvpostcmom(%cmom,1.0,hprior,bprior)

compute alpha=bdraw(1),rho=bdraw(2)

*

* After burn-in, save draws and add in the current estimate for YSTAR.

*

if draw>0 {

compute bgibbs(draw)=bdraw

set ystarhat = ystarhat+ystar

}

end do draw

infobox(action=remove)

*

@mcmcpostproc(ndraws=ndraws,mean=bmean,stderrs=bstderrs,cd=bcd) bgibbs

*

report(action=define)

report(atrow=1,atcol=1,span) "MCMC Estimates for Dynamic Probit Model"

report(atrow=2,atcol=1) "Constant" bmean(1) bstderrs(1)

report(atrow=3,atcol=1) "YSTAR{1}" bmean(2) bstderrs(2)

report(action=format,picture="*.###")

report(action=show)

*

set ystarhat = ystarhat/ndraws

*

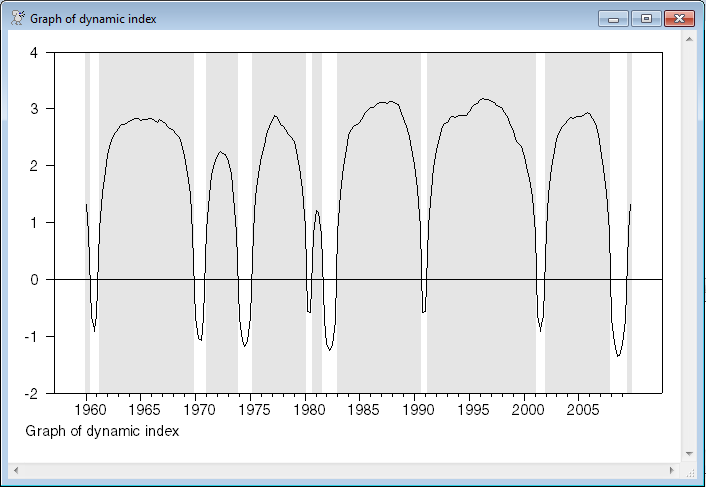

* Graph the (average across draws of the) dynamic index. Note that this is a

* "smoothed" estimate, as it uses the information from the full data set.

*

graph(shading=expansion,footer="Graph of dynamic index")

# ystarhat

Output

The MCMC estimates and the graph depend upon random numbers and so will not be exactly reproducible.

Linear Regression - Estimation by Least Squares

Dependent Variable YSTAR

Quarterly Data From 1960:02 To 2009:04

Usable Observations 199

Degrees of Freedom 197

Centered R^2 0.4705906

R-Bar^2 0.4679032

Uncentered R^2 0.7288851

Mean of Dependent Variable 0.6984924623

Std Error of Dependent Variable 0.7174222505

Standard Error of Estimate 0.5233233986

Sum of Squared Residuals 53.951873767

Regression F(1,197) 175.1128

Significance Level of F 0.0000000

Log Likelihood -152.5001

Durbin-Watson Statistic 1.7445

Variable Coeff Std Error T-Stat Signif

************************************************************************************

1. Constant 0.2193293886 0.0518397282 4.23091 0.00003564

2. YSTAR{1} 0.6859960552 0.0518397282 13.23302 0.00000000

MCMC Estimates for Dynamic Probit Model

Constant 0.353 0.124

YSTAR{1} 0.804 0.070

Graph

Copyright © 2026 Thomas A. Doan