I was inspired by chapter 7 of Rats Handbook for State-Space Models, I try to use same method to handle my situation but not sure if it‘s right.

Assuming the distributed monthly GDP data are sum to the quarterly one:

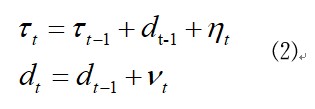

where log(I(t))=tau(t) +c(t), tau(t) is the unobserved trend, following RW(2) process:

c(t) is unobserved cycle that follow AR(2) process:

Where eta(t),nu(t),epsilon(t) all follow i.i.d normal distribution with zero mean.

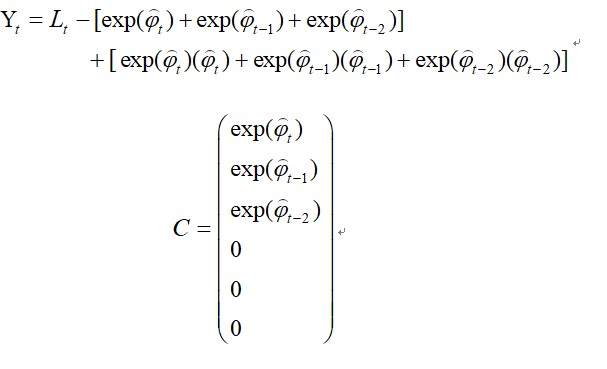

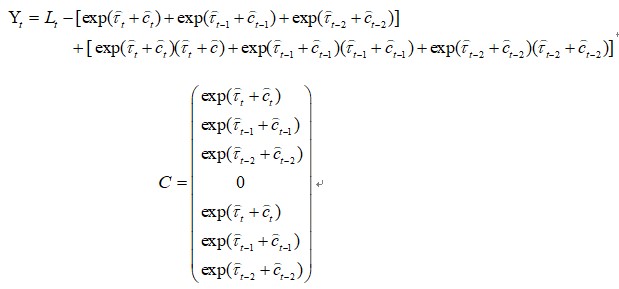

I use multi dimensional taylor expansion to handle non-linear multi-variable equation (1):

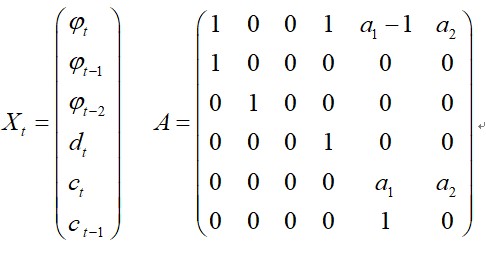

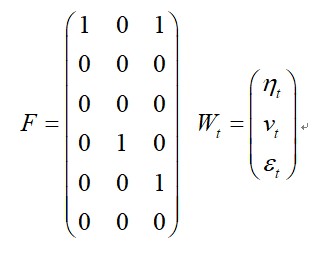

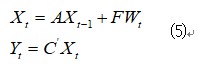

Then,I get a state space represtion of (1)-(4):

Where

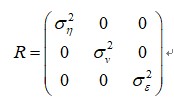

W(t) follow normal distribution with zero mean.and covariance matrix R :

Problems:

(1)Does this method work?

(2)If it works ,for iteration 1,@Disaggregate seems to set log(y*lc(i)) as first xstate0 if I'm not misunderstand, what about my situation, how to set the initial value of tau(t) & c(t) ?

Thanks in advance for any help.