|

Examples / SIMULTHEIL.RPF |

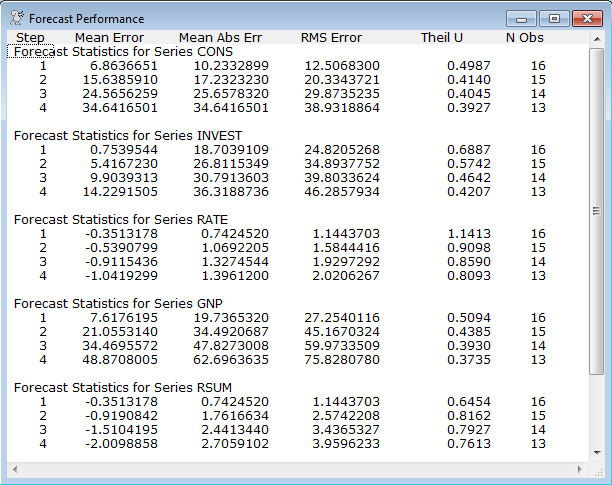

SIMULTHEIL.RPF provides an example of forecast evaluation using a simultaneous equations model.

PRSETUP.SRC reads the data and sets up the small Pindyck and Rubinfeld model.

Full Program

source prsetup.src

*

theil(setup,model=prsmall,steps=4,to=1985:4)

do time=1982:1,1985:4

theil time

end do time

theil(dump,window="Forecast Performance")

Output

Linear Regression - Estimation by Instrumental Variables

Dependent Variable CONS

Quarterly Data From 1950:01 To 1985:04

Usable Observations 144

Degrees of Freedom 141

Mean of Dependent Variable 1411.1625000

Std Error of Dependent Variable 486.7321052

Standard Error of Estimate 11.3436190

Sum of Squared Residuals 18143.554636

J-Specification(6) 57.9253

Significance Level of J 0.0000000

Durbin-Watson Statistic 1.6308

Variable Coeff Std Error T-Stat Signif

************************************************************************************

1. Constant -3.179856666 4.955717831 -0.64165 0.52213953

2. GNP 0.025662687 0.018196110 1.41034 0.16064181

3. CONS{1} 0.968332903 0.027185648 35.61927 0.00000000

Linear Regression - Estimation by Instrumental Variables

Dependent Variable INVEST

Quarterly Data From 1950:01 To 1985:04

Usable Observations 144

Degrees of Freedom 139

Mean of Dependent Variable 383.83541667

Std Error of Dependent Variable 131.09401018

Standard Error of Estimate 16.77065168

Sum of Squared Residuals 39094.411342

J-Specification(4) 25.4954

Significance Level of J 0.0000400

Durbin-Watson Statistic 2.0049

Variable Coeff Std Error T-Stat Signif

************************************************************************************

1. Constant -25.50262781 6.43431018 -3.96354 0.00011761

2. INVEST{1} 0.63725350 0.04801265 13.27262 0.00000000

3. YDIFF{1} 0.21449446 0.05425583 3.95339 0.00012218

4. GNP 0.08071954 0.01097636 7.35394 0.00000000

5. RATE{4} -4.66692377 0.98255518 -4.74978 0.00000501

Linear Regression - Estimation by Instrumental Variables

Dependent Variable RATE

Quarterly Data From 1950:01 To 1985:04

Usable Observations 144

Degrees of Freedom 139

Mean of Dependent Variable 5.1534027778

Std Error of Dependent Variable 3.2689143326

Standard Error of Estimate 0.9179997089

Sum of Squared Residuals 117.13856171

J-Specification(4) 56.2149

Significance Level of J 0.0000000

Durbin-Watson Statistic 1.4510

Variable Coeff Std Error T-Stat Signif

************************************************************************************

1. Constant 0.273120392 0.342410955 0.79764 0.42644042

2. GNP -0.000434281 0.000276810 -1.56888 0.11895023

3. YDIFF 0.022534344 0.005184064 4.34685 0.00002650

4. MDIFF -0.079425302 0.017715078 -4.48349 0.00001523

5. RSUM{1} 0.541787141 0.031239423 17.34306 0.00000000

Report

Copyright © 2026 Thomas A. Doan