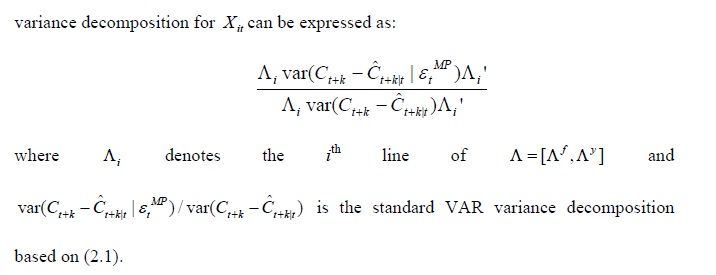

I am wondering how the variance decomposition in a Factor Augmented VAR can be calculated based on the equation below.

Source: Bernanke, Boivin and Eliasz (2003)

For example, I have a model ordered the following manner: Oil price, Activity factor (extracted from 50 variables), Price factor (extracted from 20 variables), and exchange rate. I allow variables in the activity factor to be a linear combination of oil price, activity factor, price factor and exchange rate. I am interested in the variance decomposition of GDP, which is in the activity factor. Wouldn't this just be multiplying the factor loading of GDP on each of these factors by the variance decomposition of each of these factors? That number is then divided by the overall variance that has been multipled by the loadings. But, that can result in a negative number?

Thanks.