|

Wizards / CATS Cointegration Wizard |

CATS (Cointegration Analysis of Time Series) is an add-on package available for RATS that implements a sophisticated, menu- and window-driven suite of cointegration analysis and testing procedures. If you have Version 2.0 or later of CATS, you can use the CATS Wizard to start the CATS procedure.

Note: In order for the Wizard to function properly, you must have the CATS Directory field on the Directories tab of the File>Preferences dialog set properly, so that RATS can locate the CATS procedure files.

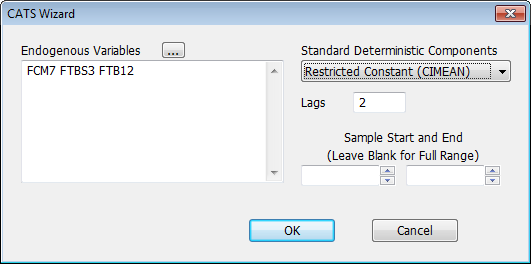

Selecting the CATS Cointegration Wizard from the Time Series Menu brings up the following dialog box, which allows you to set some of the basic parameters for the CATS model. When you click OK, RATS will source in the CATS procedures and start CATS using the settings you requested. You will see some initial output in the output window, and the various CATS menus will be added to the RATS menu bar. See the CATS manual for more information on using CATS. (The wizard dialog is deceptively simple since most of the interesting work is done using the menus and dialogs that CATS itself brings up).

Endogenous Variable(s)

Use this field to define the endogenous variables for the model. You can either type in a list of endogenous variables, separating variables with at least one blank space, or click on the series list button ![]() to select from a list of the series available in memory with a Select Variables dialog box.

to select from a list of the series available in memory with a Select Variables dialog box.

Standard Deterministic Components

Use this field to select the basic deterministic variable structure. The choices are "None", "Restricted Constant (CIMEAN)", "Unrestricted Constant (DRIFT)", or "Restricted Trend".

Lags

Enter a single integer value to specify the lag length.

Sample Start and End

Use these fields to set a specific starting and/or ending date for the estimation.

Note that some of the settings can be changed from within CATS once the procedure has been started. For example, you can use the Model operation on the main CATS menu to alter the deterministic variables and lag structure or to add seasonal terms.

Copyright © 2026 Thomas A. Doan