Dear Tom,

I estimated a model using Gray's code. Here is the results. Is there enough evidence about the existence of second regime?

I don't know why P(1,2) is such low. What does is mean here? Especially, why is A12 greater than minus one? Does it has show that something is wrong with the model?

Linear Regression - Estimation by Least Squares

With Heteroscedasticity-Consistent (Eicker-White) Standard Errors

Dependent Variable DRATE

Daily(5) Data From 2003:01:06 To 2012:12:06

Usable Observations 2589

Degrees of Freedom 2587

Centered R^2 0.2162382

R-Bar^2 0.2159353

Uncentered R^2 0.2162382

Mean of Dependent Variable -0.000019215

Std Error of Dependent Variable 0.710001062

Standard Error of Estimate 0.628687695

Sum of Squared Residuals 1022.5071405

Log Likelihood -2471.0231

Durbin-Watson Statistic 2.3494

Variable Coeff Std Error T-Stat Signif

************************************************************************************

1. Constant 0.000001372 0.012350981 1.11101e-004 0.99991135

2. DRATE{1} -0.465022692 0.029848275 -15.57955 0.00000000

MAXIMIZE - Estimation by BFGS

Convergence in 14 Iterations. Final criterion was 0.0000048 <= 0.0000100

Daily(5) Data From 2003:01:03 To 2012:12:06

Usable Observations 2590

Function Value -1233.4961

Variable Coeff Std Error T-Stat Signif

************************************************************************************

1. A01 0.034373643 0.016306202 2.10801 0.03503009

2. A02 -0.018158900 0.005627435 -3.22685 0.00125160

3. A11 -0.987049117 0.024645457 -40.04994 0.00000000

4. A12 -1.036718008 0.031279355 -33.14384 0.00000000

5. B01 0.676242638 0.013864548 48.77495 0.00000000

6. B02 0.178090890 0.005701714 31.23462 0.00000000

7. P(1,1) 0.964435993 0.006934697 139.07400 0.00000000

8. P(1,2) 0.038301809 0.005753795 6.65679 0.00000000

Lag Corr Partial LB Q Q Signif

1 0.089 0.089 20.64769 0.0000

2 0.309 0.303 268.42934 0.0000

3 0.122 0.084 307.28896 0.0000

4 0.101 -0.003 333.89765 0.0000

5 0.082 0.018 351.45483 0.0000

6 0.031 -0.013 354.02735 0.0000

7 0.044 0.006 359.06825 0.0000

8 0.022 0.006 360.29757 0.0000

9 0.055 0.041 368.24714 0.0000

10 0.052 0.040 375.21940 0.0000

11 0.068 0.039 387.30424 0.0000

12 0.089 0.056 408.03453 0.0000

13 0.072 0.028 421.61656 0.0000

14 0.111 0.057 453.70138 0.0000

15 0.091 0.043 475.14533 0.0000

GARCH Model - Estimation by BFGS

Convergence in 31 Iterations. Final criterion was 0.0000059 <= 0.0000100

Dependent Variable DRATE

Daily(5) Data From 2003:01:06 To 2012:12:06

Usable Observations 2589

Log Likelihood -1640.8258

Variable Coeff Std Error T-Stat Signif

************************************************************************************

1. Constant -0.002580050 0.004870402 -0.52974 0.59629165

2. DRATE{1} -0.486710196 0.017265759 -28.18933 0.00000000

3. C 0.001934000 0.000469922 4.11558 0.00003862

4. A 0.318002213 0.026901340 11.82105 0.00000000

5. B 0.744130400 0.017127159 43.44739 0.00000000

Lag Corr Partial LB Q Q Signif

1 -0.031 -0.031 2.552248 0.1101

2 0.070 0.069 15.294223 0.0005

3 -0.028 -0.024 17.282169 0.0006

4 -0.015 -0.021 17.855229 0.0013

5 -0.039 -0.037 21.893056 0.0005

6 -0.043 -0.043 26.625084 0.0002

7 -0.036 -0.035 30.074676 0.0001

8 -0.038 -0.037 33.871933 0.0000

9 -0.032 -0.034 36.612003 0.0000

10 -0.001 -0.003 36.617247 0.0001

11 -0.022 -0.025 37.857947 0.0001

12 -0.011 -0.021 38.194854 0.0001

13 -0.012 -0.017 38.548140 0.0002

14 -0.029 -0.037 40.769661 0.0002

15 0.002 -0.006 40.779242 0.0003

MAXIMIZE - Estimation by BFGS

Convergence in 9 Iterations. Final criterion was 0.0000091 <= 0.0000100

Daily(5) Data From 2003:01:03 To 2012:12:06

Usable Observations 2590

Function Value -1054.8672

Variable Coeff Std Error T-Stat Signif

************************************************************************************

1. A01 0.013619894 0.013106682 1.03916 0.29873196

2. A02 -0.014933917 0.004393704 -3.39894 0.00067649

3. A11 -0.935668475 0.028987754 -32.27806 0.00000000

4. A12 -1.064079366 0.034639104 -30.71902 0.00000000

5. B01 0.067855137 0.006098469 11.12659 0.00000000

6. B11 0.136280582 0.028697956 4.74879 0.00000205

7. B21 0.807379310 0.029557752 27.31532 0.00000000

8. B02 0.003801359 0.000683465 5.56189 0.00000003

9. B12 0.310732981 0.049463576 6.28206 0.00000000

10. B22 0.292483566 0.028278038 10.34313 0.00000000

MAXIMIZE - Estimation by BFGS

Convergence in 21 Iterations. Final criterion was 0.0000094 <= 0.0000100

Daily(5) Data From 2003:01:03 To 2012:12:06

Usable Observations 2590

Function Value -1050.5437

Variable Coeff Std Error T-Stat Signif

************************************************************************************

1. A01 0.010285521 0.012745732 0.80698 0.41967938

2. A02 -0.015746220 0.004411478 -3.56937 0.00035783

3. A11 -0.934642290 0.030346397 -30.79912 0.00000000

4. A12 -1.085577499 0.037463795 -28.97671 0.00000000

5. B01 0.050692332 0.009910202 5.11517 0.00000031

6. B11 0.157356240 0.031981527 4.92022 0.00000086

7. B21 0.802614140 0.049317631 16.27439 0.00000000

8. B02 0.003374801 0.001166368 2.89343 0.00381063

9. B12 0.229441167 0.070668669 3.24672 0.00116744

10. B22 0.246944292 0.038749720 6.37280 0.00000000

11. P(1,1) 0.960576407 0.013708449 70.07185 0.00000000

12. P(1,2) 0.075710440 0.020554312 3.68343 0.00023011

MAXIMIZE - Estimation by BFGS

NO CONVERGENCE IN 12 ITERATIONS

LAST CRITERION WAS 0.0000000

SUBITERATIONS LIMIT EXCEEDED.

ESTIMATION POSSIBLY HAS STALLED OR MACHINE ROUNDOFF IS MAKING FURTHER PROGRESS DIFFICULT

TRY HIGHER SUBITERATIONS LIMIT, TIGHTER CVCRIT, DIFFERENT SETTING FOR EXACTLINE OR ALPHA ON NLPAR

RESTARTING ESTIMATION FROM LAST ESTIMATES OR DIFFERENT INITIAL GUESSES MIGHT ALSO WORK

Daily(5) Data From 2003:01:03 To 2012:12:06

Usable Observations 2590

Function Value -1018.0690

Variable Coeff Std Error T-Stat Signif

************************************************************************************

1. A01 -0.013393998 0.000380707 -35.18194 0.00000000

2. A02 0.045332574 0.002076028 21.83620 0.00000000

3. A11 -1.097700039 0.005548809 -197.82625 0.00000000

4. A12 -0.303118795 0.027167144 -11.15755 0.00000000

5. B01 -0.001011178 0.000002767 -365.49626 0.00000000

6. B11 0.059900700 0.000807929 74.14101 0.00000000

7. B21 0.609069171 0.000384612 1583.59479 0.00000000

8. B02 0.019938741 0.000145776 136.77666 0.00000000

9. B12 0.045280994 0.000174983 258.77336 0.00000000

10. B22 1.870801841 0.029521412 63.37101 0.00000000

11. P(1,1) 0.820696725 0.000355251 2310.18726 0.00000000

12. P(1,2) 0.723588475 0.006872191 105.29226 0.00000000

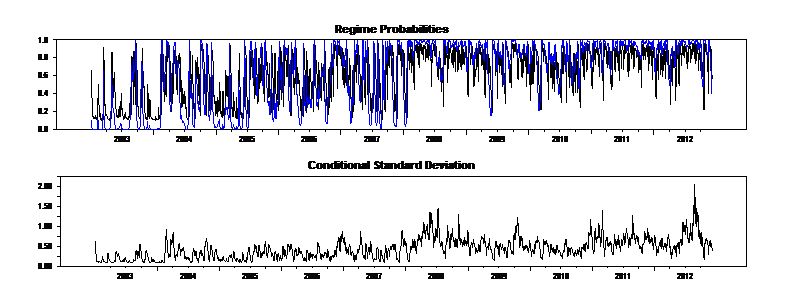

And here is ex ante and smoothed probabilities:

- figure 5.png (28.08 KiB) Viewed 58933 times

Here is the code:

Code: Select all

All of this was out of Gray's paper, "Modeling the conditional

* distribution of interest rates as a regime-switching process", J. of

* Financial Economics 42, 1996, pp 27-62.

*

* Revision Schedule:

* 01/2005 Written by Tom Doan, Estima

* 09/2005 Comments added. Changed to use new %MSSMOOTH procedure

*

OPEN DATA data.xlsx

CALENDAR(D) 2003:1:2

all 2012:12:06

DATA(FORMAT=XLSX,ORG=COLUMNS) 2003:01:02 2012:12:06 rupee rate

set rate = rate*100.0

diff rate / drate

spgraph(vfields=2,window="Figure 3")

graph(header="One Month T-Bill Rates")

# rate

graph(header="One Month T-Bill Yields")

# drate

spgraph(done)

*

* This makes extensive use of the Markov switching functions and

* procedures from MSSetup.src

*

@MSSetup(states=2)

*

* The P and Q values in Gray's notation are handled in MSSetup as an M-1

* x M matrix (called P here), with P(i,j) giving the probabilities of

* moving from state j to state i. The Mth row is implicit, as it's just

* the 1-sum of rest of the column.

*

*******************************************************************************

*

* Table 1 information

*

stats drate

cmom(corr,print)

# drate rate{1}

*******************************************************************************

*

* Table 2 estimates

*

* Single regime is linear regression

*

linreg(robust) drate

# constant drate{1}

*

* We're going to use these later for initial conditions

*

compute olsvar =%seesq

compute olsbeta=%beta

*

* Constant variance regime switching model

* This uses Gray's notation for all the variables other than "P"

*

nonlin a01 a02 a11 a12 b01 b02 p

*

* Initial guess values for MS models are always a bit tricky because the

* model isn't globally identified. This is starting with OLS results for

* state 1 and 0 mean coefficients for state 2.

*

compute a01=olsbeta(1),a11=olsbeta(2),b01=sqrt(olsvar)

compute a02=a12=0.0,b02=b01

*

* The p matrix is initialized to make both states fairly persistent.

* (The 2,2 transition is 1-.1=.9).

*

compute p=||.8,.1||

*

* SimpleRegimeF returns the 2-vector of densities in the two regimes. It

* is specific to the data series used (dependent variable <<drate>>) and

* the precise parameterization, and so would need to be altered slightly

* for a different application. Note that this needs to return the actual

* density, not its log.

*

function SimpleRegimeF t

type vector SimpleRegimeF

type integer t

*

compute SimpleRegimeF=||%density((drate(t)-a01-a11*rate(t-1))/b01)/b01,$

%density((drate(t)-a02-a12*rate(t-1))/b02)/b02||

end

*

* This is the standard log likelihood FRML for a Markov switching model.

*

frml logl = f=SimpleRegimeF(t),fpt=%MSProb(t,f),log(fpt)

@MSFilterInit

maximize(start=(pstar=%MSInit()),method=bfgs,iters=100,pmethod=simplex,piters=5) logl 2 2012:12:06

*

* It's not clear what residuals are used for the diagonostics for the

* regime switching model. The standardized residuals weighted by the ex

* ante probabilities of the two states seem to give LB's which are

* fairly close to those in the paper.

*

set ustd = %dot(pt_t1,||(drate-a01-a11*drate{1})/b01,(drate-a02-a12*drate{1})/b02||)

graph

# ustd

set usqr = ustd^2

@regcorrs(report,number=15) usqr

*

* Compute the smoothed probabilities and the ex ante probabilities

*

@MSSmoothed %regstart() %regend() psmooth

set exante %regstart() %regend() = pt_t1(t)(1)

set smooth %regstart() %regend() = psmooth(t)(1)

*

* And the conditional standard deviation

*

set condstddev = sqrt(exante*b01^2+(1-exante)*b02^2)

*

spgraph(vfields=2,window="Figure 4")

graph(max=1.0,header="Regime Probabilities") 2

# exante

# smooth

graph(header="Conditional Standard Deviation")

# condstddev

spgraph(done)

*******************************************************************************

*

* Table 3 estimates

*

* Single regime GARCH model

*

garch(p=1,q=1,reg,resids=u,hseries=h) / drate

# constant drate{1}

compute onestate=%beta

*

set usqr = u^2/h

@regcorrs(number=15,report) usqr

*

* Regime-switching GARCH

*

nonlin a01 a02 a11 a12 b01 b11 b21 b02 b12 b22 p

compute a01=%beta(1),a11=%beta(2),b01=olsvar,b11=0.0,b21=0.0

compute a02=%beta(1),a12=%beta(2),b02=%beta(3),b12=%beta(4),b22=%beta(5)

compute p=||.95,.05||

*

set uu = olsvar

set h = olsvar

*

* RegimeGARCHF returns the 2 vector of densities in the two regimes.

* Again, many lines in this are specific to the problem at hand.

*

function RegimeGARCHF t

type vector RegimeGARCHF

type integer t

local real hh1 hh2 mu1 mu2 mu

*

* Compute state dependent variances

*

compute hh1=b01+b11*uu(t-1)+b21*h(t-1)

compute hh2=b02+b12*uu(t-1)+b22*h(t-1)

*

* Compute state dependent means

*

compute mu1=a01+a11*rate(t-1)

compute mu2=a02+a12*rate(t-1)

*

* Compute the return vector (densities in the two states)

*

compute RegimeGARCHF=||%density((drate(t)-mu1)/sqrt(hh1))/sqrt(hh1),$

%density((drate(t)-mu2)/sqrt(hh2))/sqrt(hh2)||

*

* Compute the values of uu (squared residual) and h (variance) to be

* used for the period following.

*

compute mu=mu1*pstar(1)+mu2*pstar(2)

compute uu(t)=(drate(t)-mu)^2

compute h(t)=pstar(1)*(mu1^2+hh1)+pstar(2)*(mu2^2+hh2)-mu^2

end

*

frml logl = f=RegimeGARCHF(t),fpt=%MSProb(t,f),log(fpt)

*

* This combination is able to locate Gray's results - the first MAXIMIZE

* works with the "p" matrix fixed at a fairly high level of persistence,

* and tries to get estimates which separate the two states. The second

* then adds the p matrix to the parmset.

*

nonlin a01 a02 a11 a12 b01 b11 b21 b02 b12 b22

maximize(start=(pstar=%MSInit()),method=bfgs,iters=100,pmethod=simplex,piters=50) logl 2 2012:12:06

nonlin a01 a02 a11 a12 b01 b11 b21 b02 b12 b22 p

maximize(start=(pstar=%MSInit()),method=bfgs,iters=100) logl 2 2012:12:06

*

* Compute the smoothed probabilities and the ex ante probabilities

*

@MSSmoothed %regstart() %regend() psmooth

set exante %regstart() %regend() = pt_t1(t)(1)

set smooth %regstart() %regend() = psmooth(t)(1)

*

* And the conditional standard deviation

*

set condstddev = sqrt(h)

*

spgraph(vfields=2,window="Figure 5")

graph(max=1.0,header="Regime Probabilities") 2

# exante

# smooth

graph(header="Conditional Standard Deviation")

# condstddev

spgraph(done)

*

*

* However, this set of initial guess values (which are actually the

* result of a typo in trying to reproduce the article's numbers) find a

* local max with quite a bit higher likelihood, and dramatically

* different behavior. How one might find this systematically is unclear.

*

compute a01=.1407,a02=-.0011,a11=-.0141,a12=.0006,b01=.0004,b11=.4609,b21=.1977,b02=.0099,b12=.1655,b22=.2685,p=||.9739,1-.9896||

maximize(start=(pstar=%MSInit()),method=bfgs,iters=100,pmethod=simplex,piters=50) logl 2 2012:12:06

*******************************************************************************